by: Zach Bethune, Thomas Cooley, Peter Rupert

The Bureau of Labor Statistics release of the October jobs report showed continued steady improvement in the US labor market. Total non-farm payroll employment increased by 214,000, just slightly below the average monthly gain of 222,000 observed over the previous twelve months. Moreover, September employment gains were revised up by 8,000.

While the gains were broad-based, the bulk of the increase occurred in private service sector at 181,000. Employers are increasing their work force at both the extensive margin (jobs) and the intensive margin (hours). Average weekly hours increased slightly as did average hourly earnings.

The official unemployment rate moved down to 5.8%, the lowest rate since July, 2008, and the U-6 rate (Total unemployed, plus all persons marginally attached to the labor force, plus total employed part time for economic reasons, as a percent of the civilian labor force plus all persons marginally attached to the labor force) fell to 11.5%. The employment to population ratio and labor force participation increased.

Transition Rate Up for Long-term Unemployed…

While the median unemployment duration ticked up in October from 31.5 to 32.7 weeks, the rate at which workers are finding jobs has shown steady improvement. Since early 2014, the unemployment to employment transition rate has increased for all workers, particularly for those unemployed less than 14 weeks.

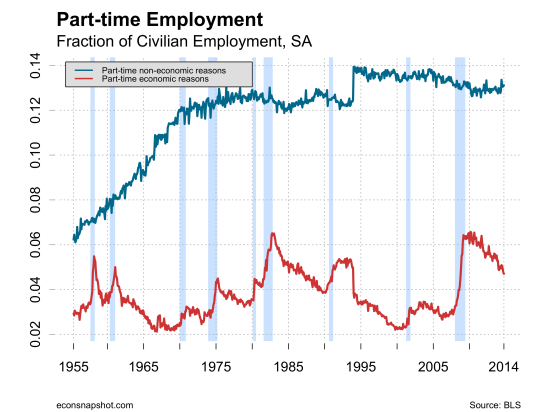

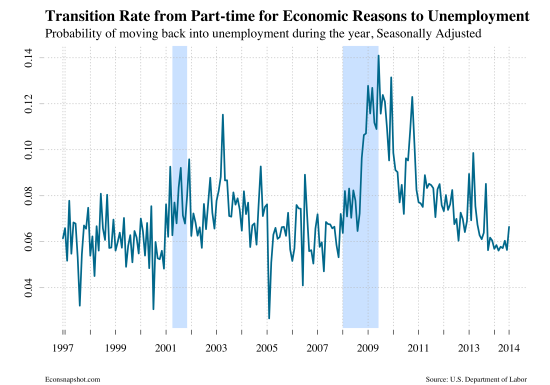

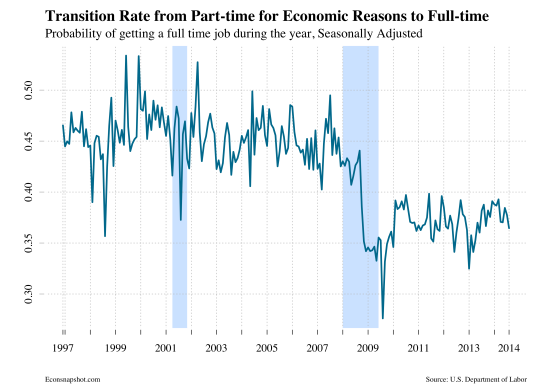

The number of employees working part-time for economic reasons (PTER) has also declined as the number of persons stating they could only find part-time employment fell by 115,000. This group of workers has been a focus of the Fed in describing the ‘slack’ still existent in the labor market.

In the figures below, we show the rate at which these workers either return to unemployment or find full-time work. The transition rate into unemployment has entirely returned to its pre-recession level. PTER workers are not losing their jobs as frequently as during the depths of the recession. However, we do still see that these workers aren’t finding full-time employment at the rate they once did before 2007. In fact, the transition rate from PTER into full-time employment hasn’t shown any signs of improving in the previous 5 years, despite accommodative monetary policy.

This is all evidence of a healthy, recovering labor market. Some of the overhang of the great recession will be with us for a long time. For instance, people unemployed for long durations are going to move only very slowly back to employment because long spells of unemployment erode skills and diminish employability. Stimulus policies will not impact these workers very much – only targeted skill building programs will.

A Fed Call to Arms?

Given that the labor market now seems reliably recovered and GDP growth is steadily positive it seems to be time for Fed to put aside its fear of the consequences and restore normalcy to monetary policy. It is important not only because of the dangers of waiting too long but also because of the hidden costs of the current policy. Keeping the Federal Funds rate at zero for an extended period has distorted economic decisions and financial markets as investors search for yield and seem to take on more risk. It has also arguably increased income inequality precisely because of the wealth effect the policy was designed to create. Moving back to a normal monetary policy need not be disruptive and should enhance the Fed’s credibility going forward. The graph below shows the Federal Funds rate implied by the Fed’s earlier announced goal of a 6.5% unemployment rate. While everyone realizes that is not the current goal it illustrates the case for a return to conventional monetary policy.

{kind=link}