By Thomas Cooley and Peter Rupert

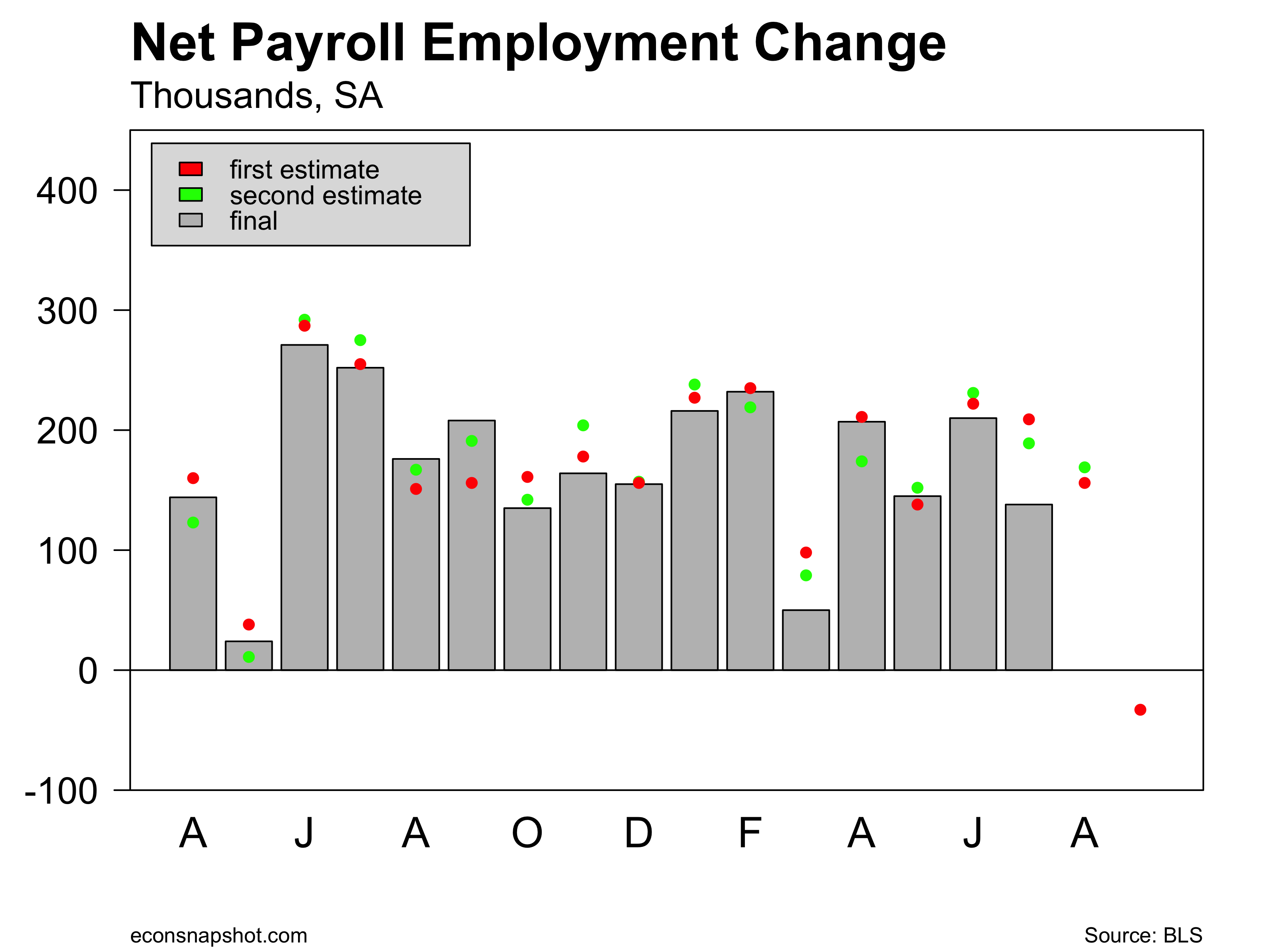

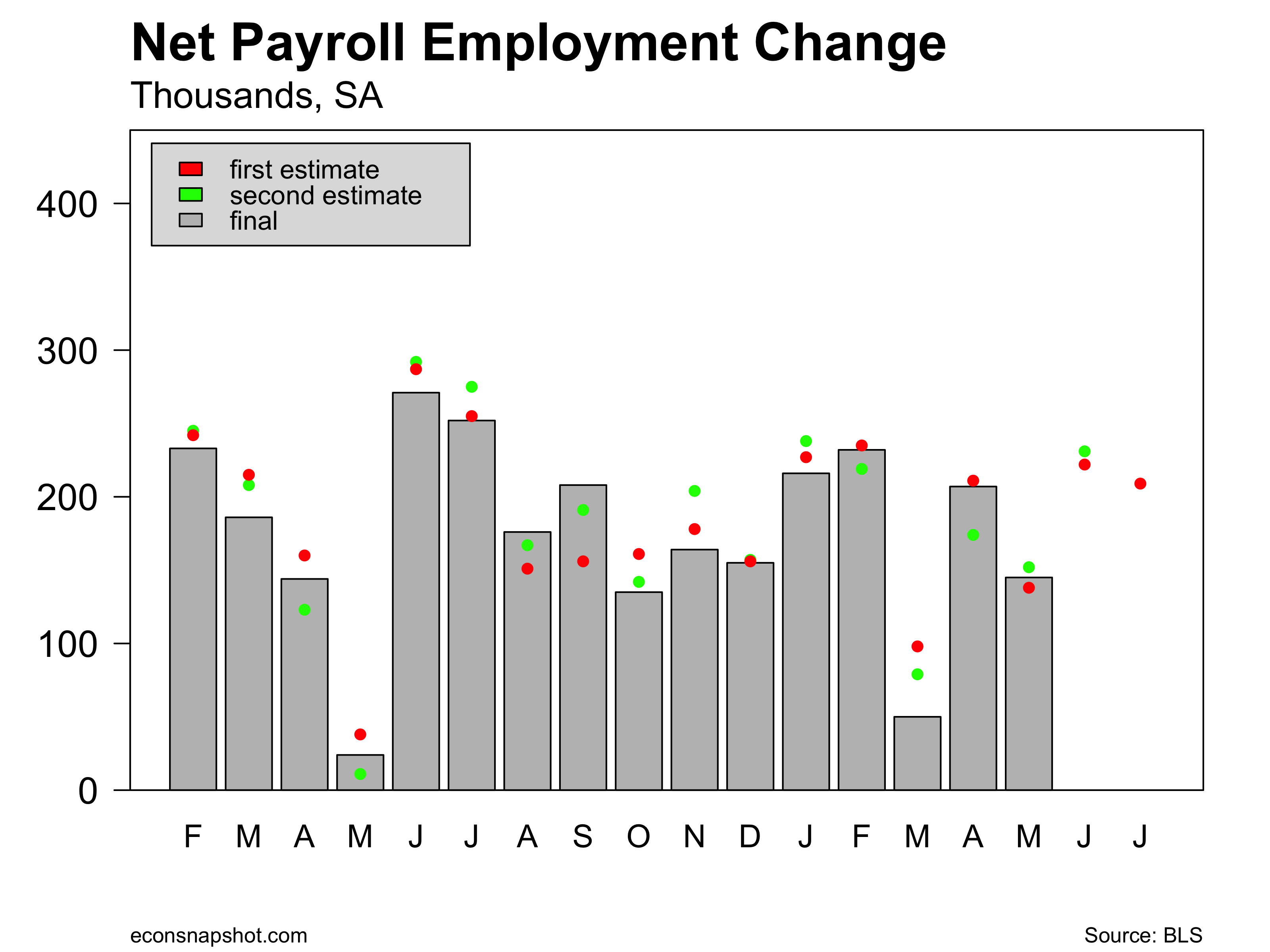

The June jobs report was stronger than many people expected given that other economic indicators for the second quarter have been soft. The BLS data show an increase in payroll employment of 222,000 with upward revisions of 14,000 for May and 33,000 for April. The average number of jobs added in the private sector is 180,000 per month in 2017, just slightly less than the 187,00 per month added in 2016. The service sector provided 162,000 additional jobs. The largest contributors in the service sector were Health Care and Social Assistance which added 59,000 jobs, and Professional and Business Services, up 35,000.

The volatile Mining sector continues to expand, up 8,000. Manufacturing and Construction employment are still nearly 10% below the level back in January, 2008.

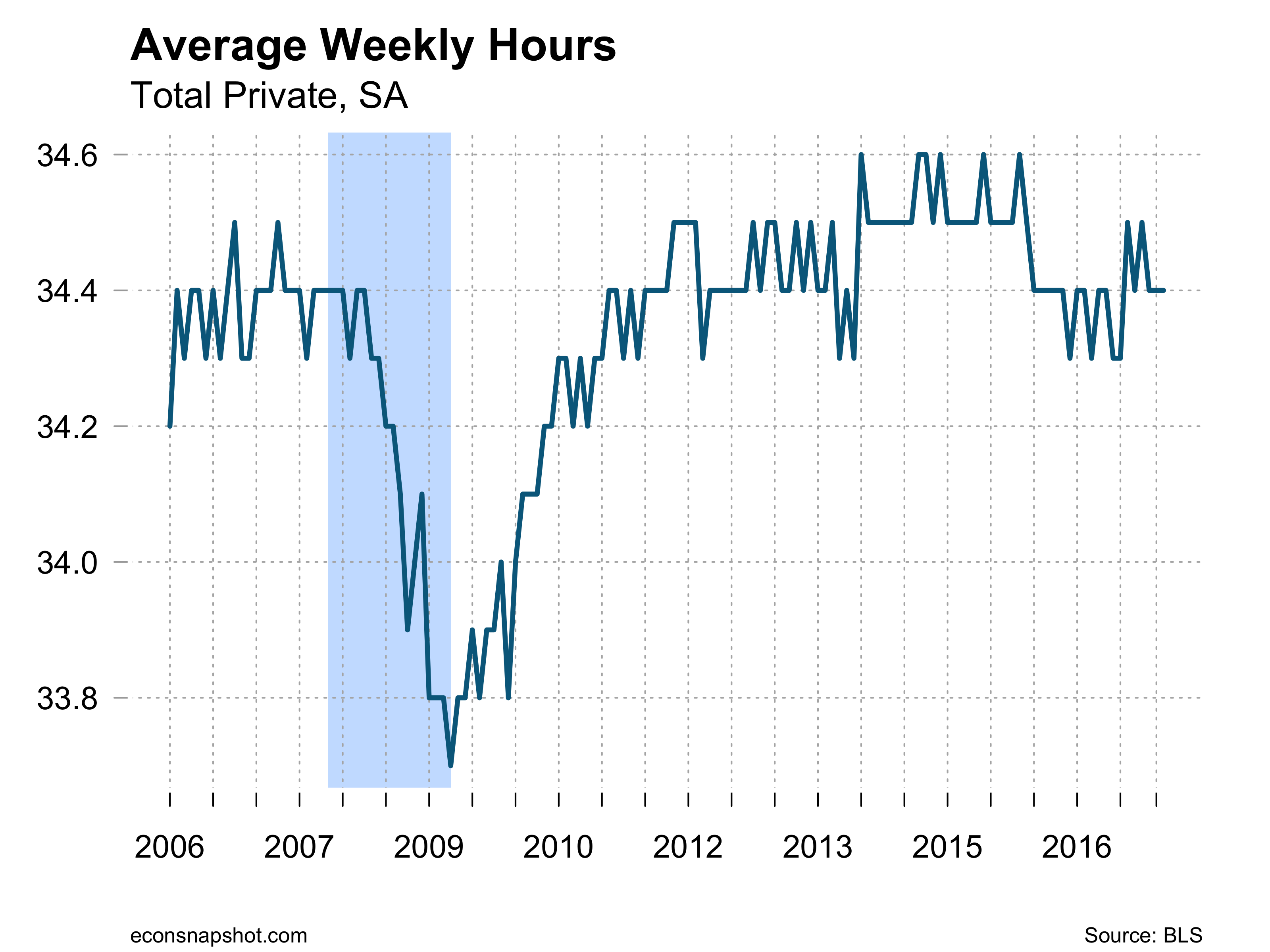

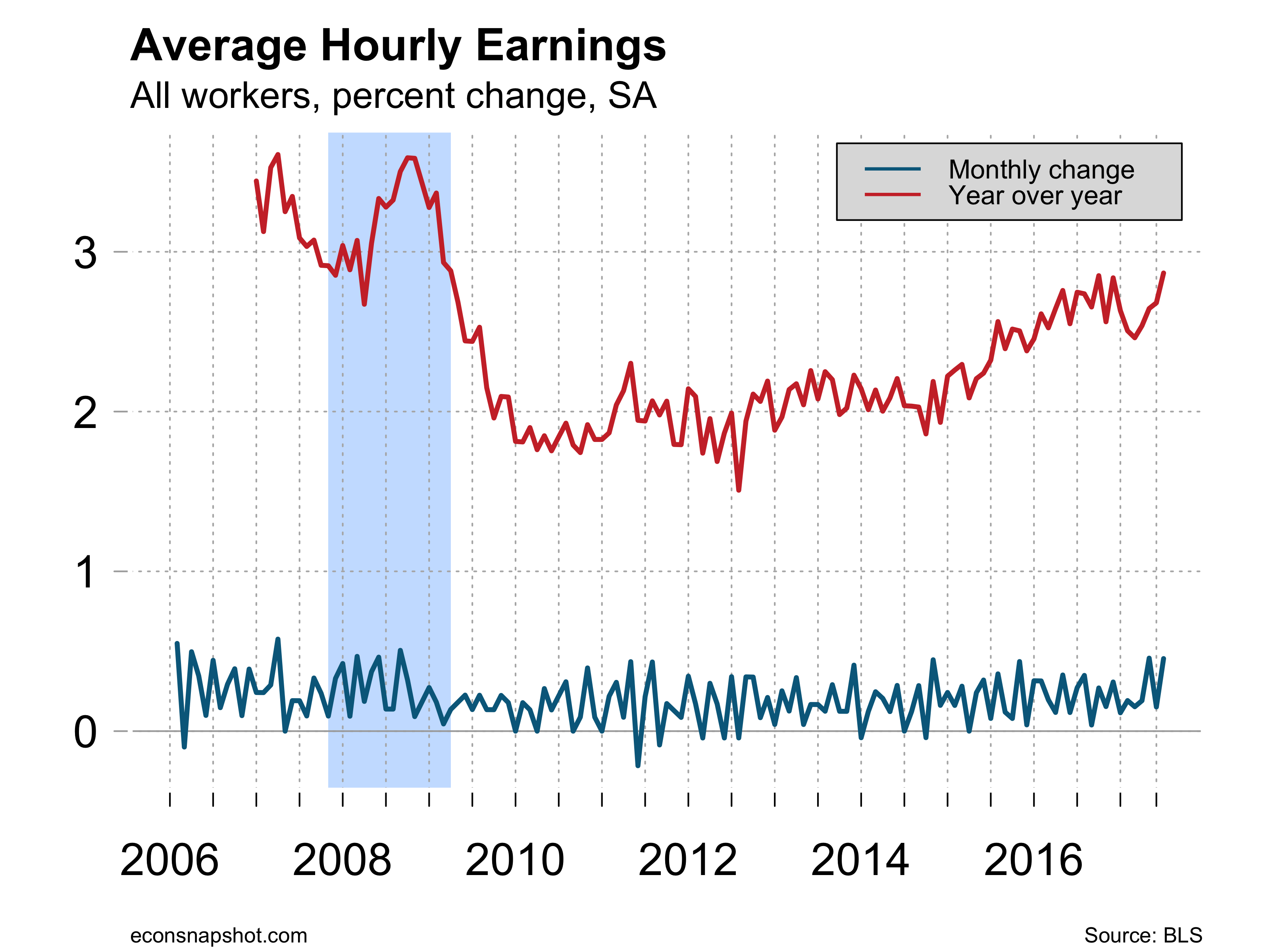

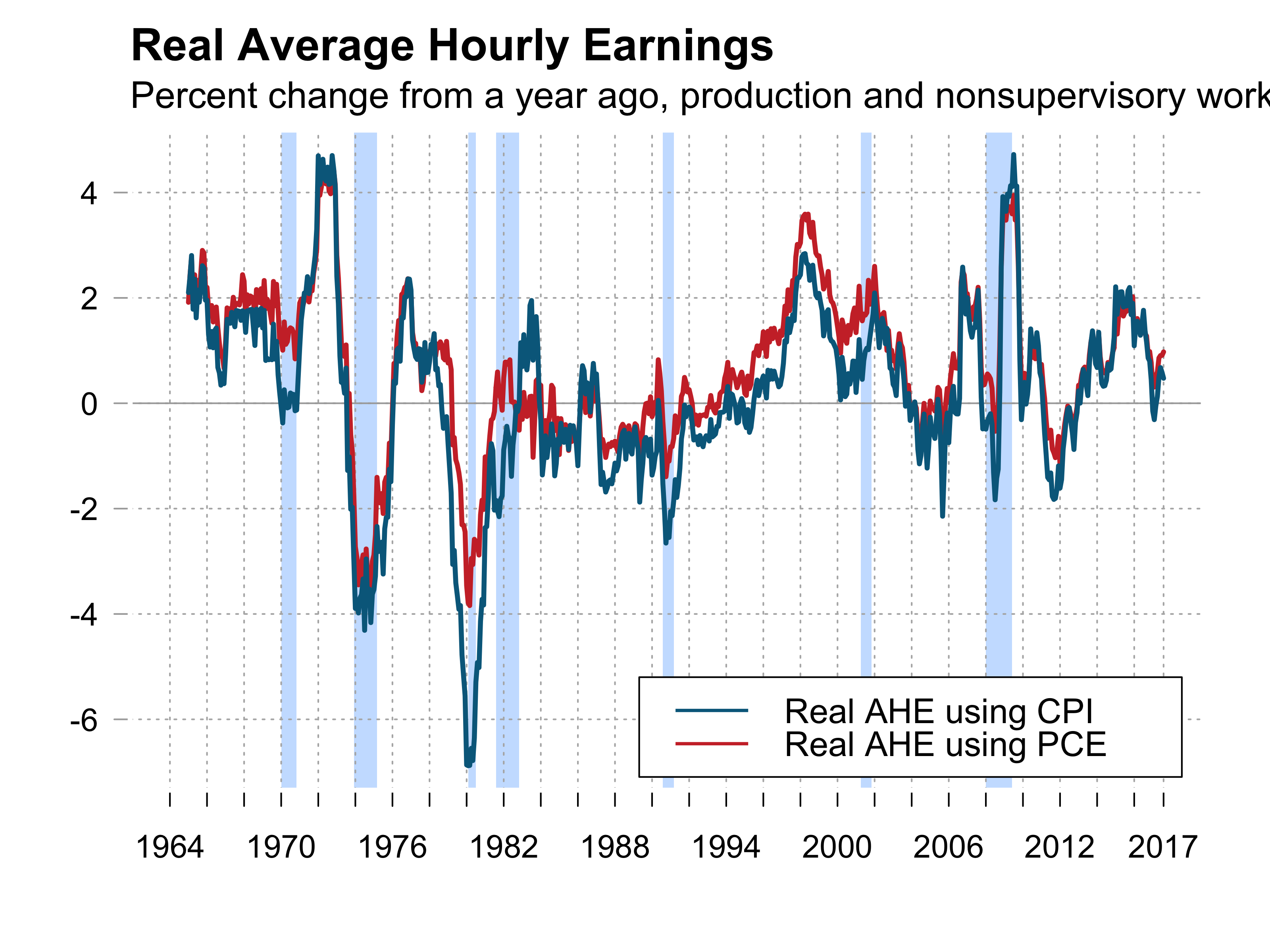

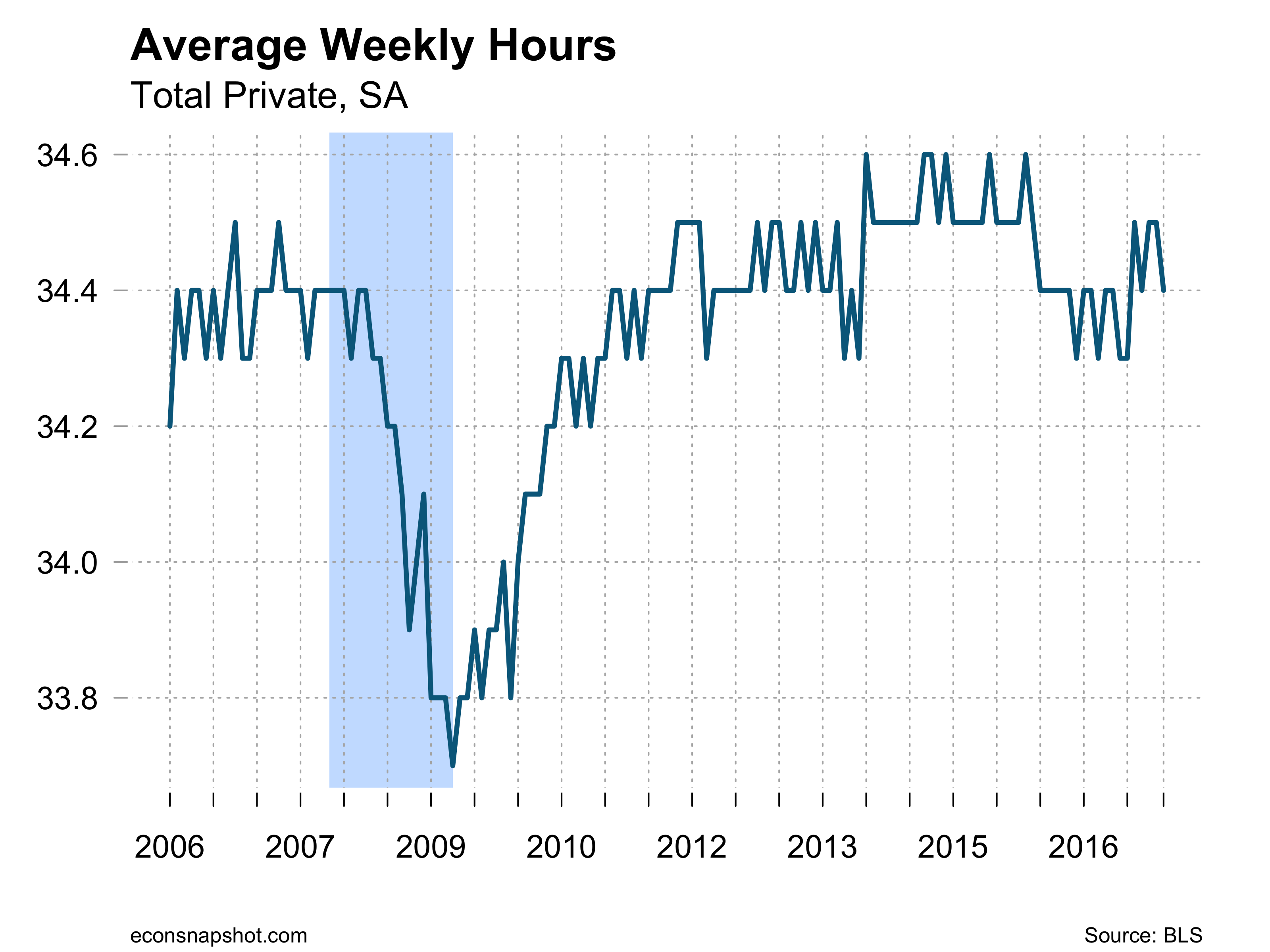

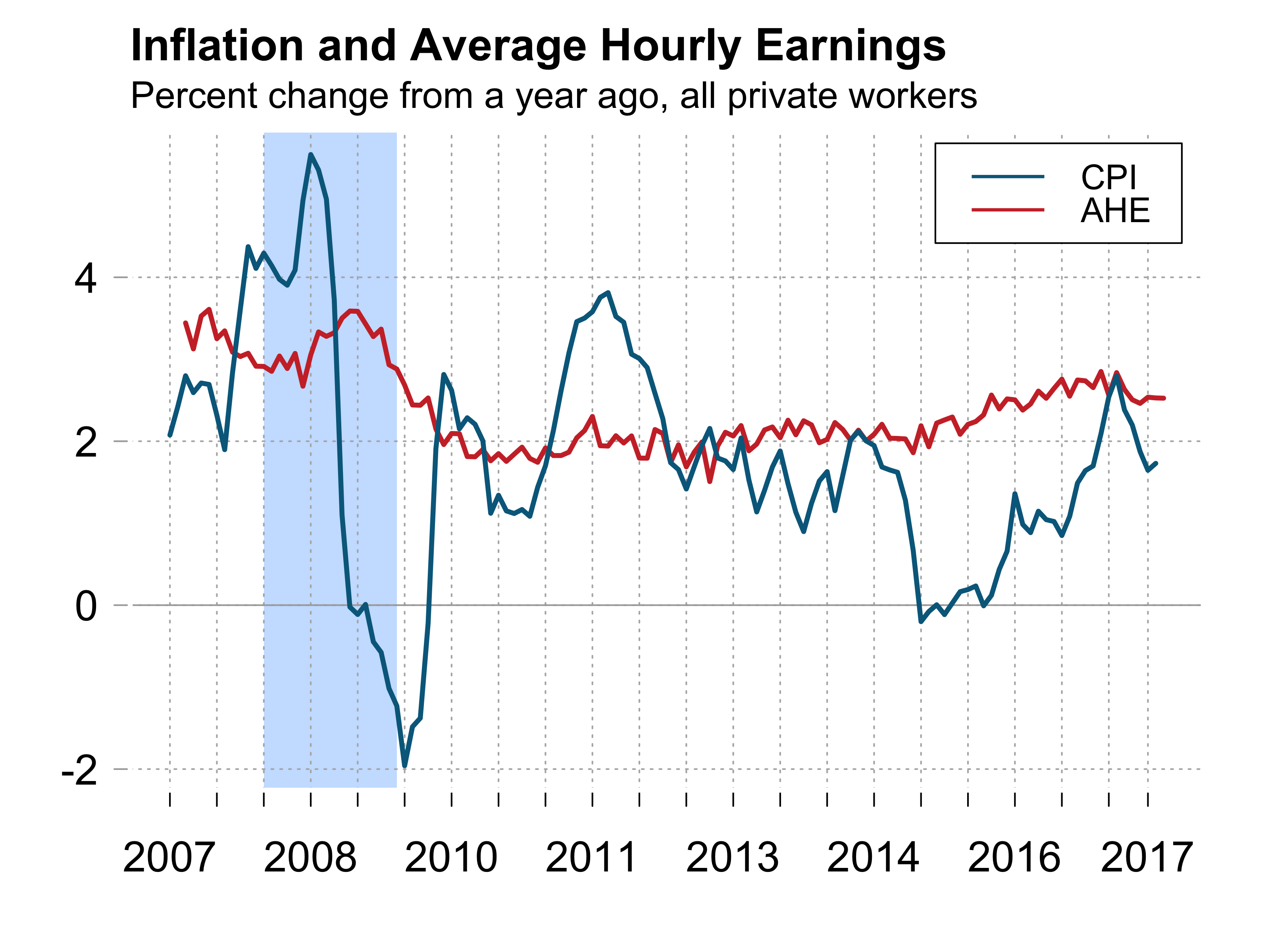

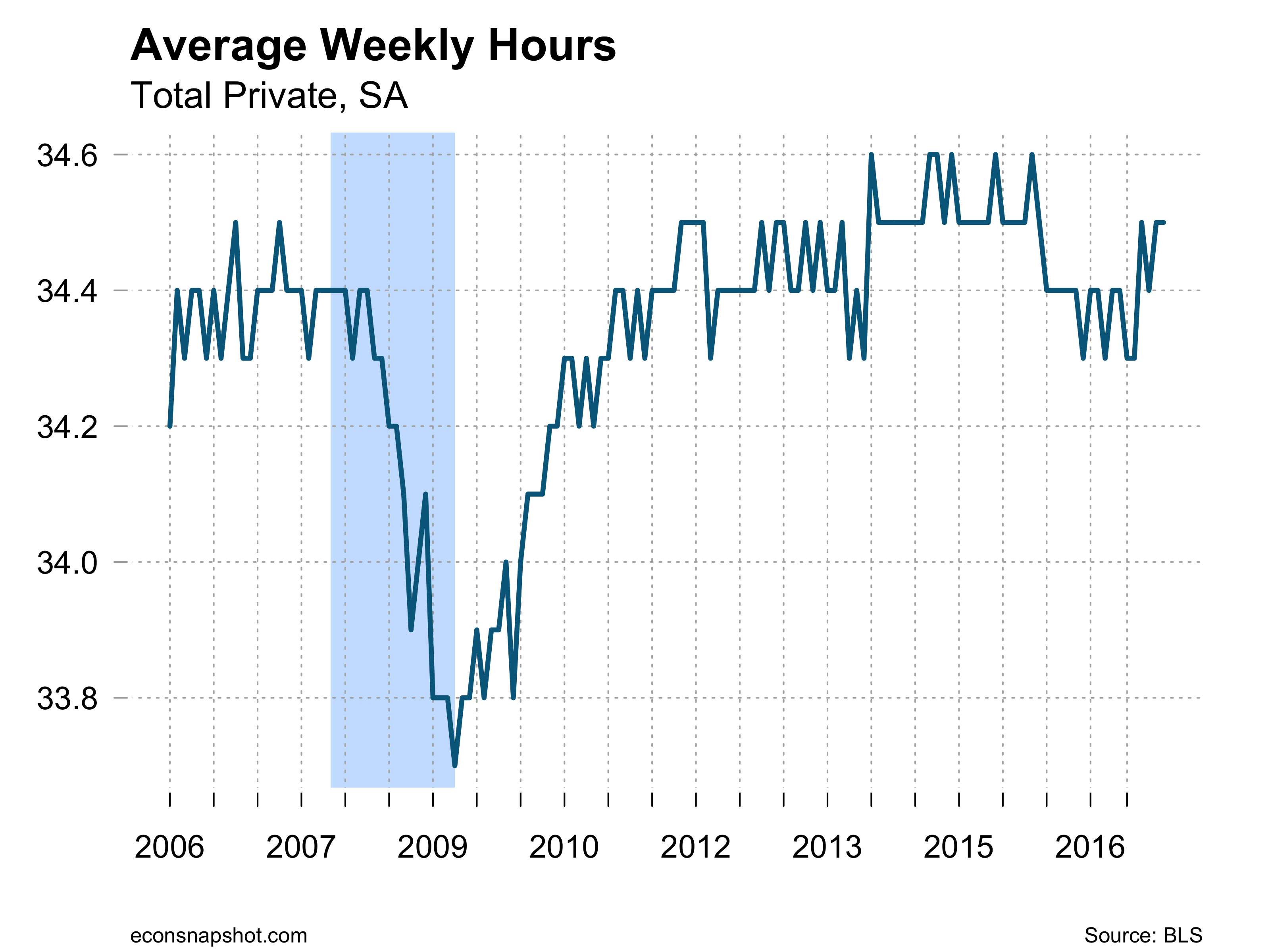

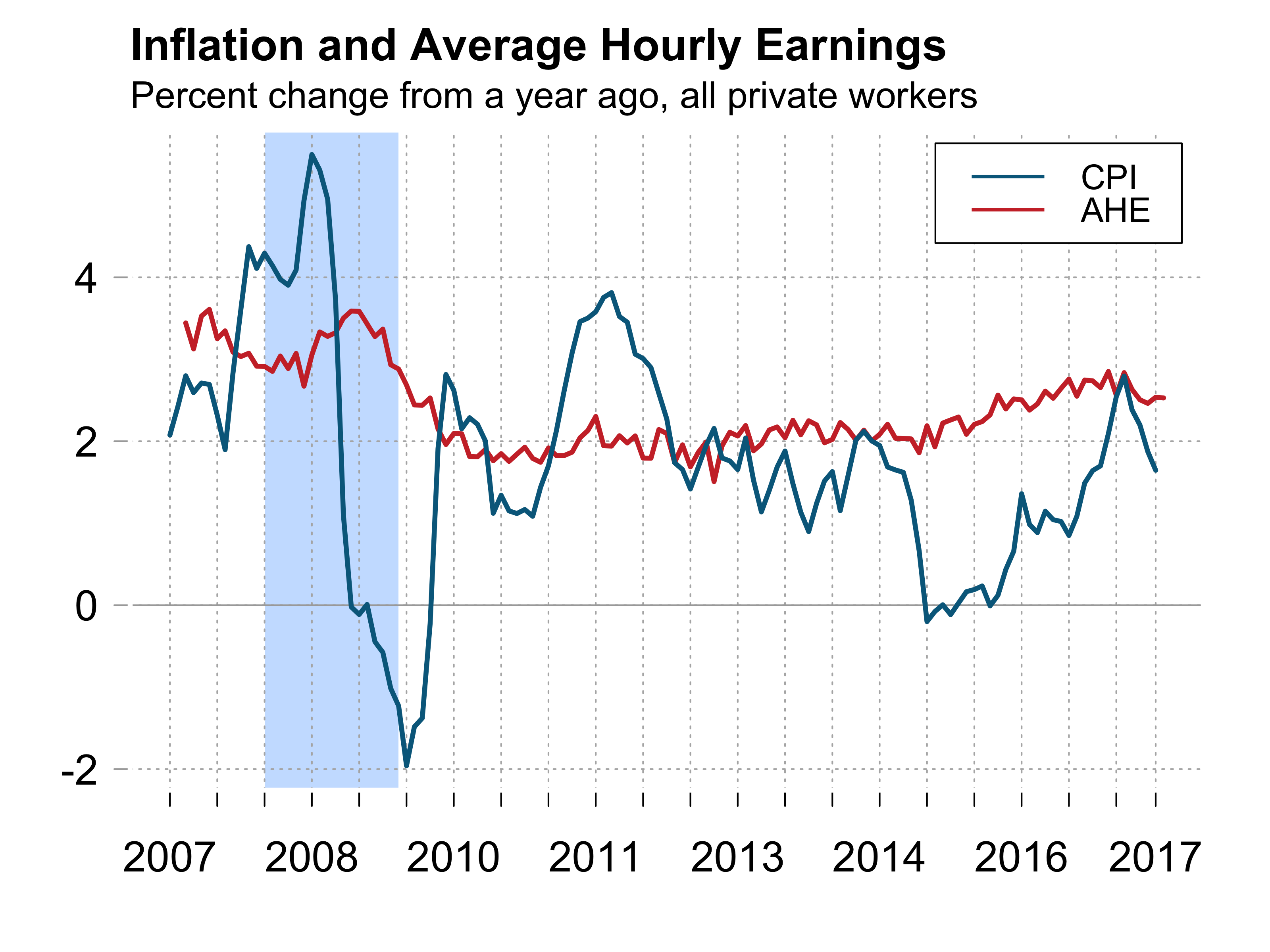

The household data indicates average weekly hours remained at 34.4 and average hourly earnings ticked up by only 4 cents last month and is up 2.5% since June of last year. With inflation up 1.87% since June of last year, real average earnings are up only slightly.

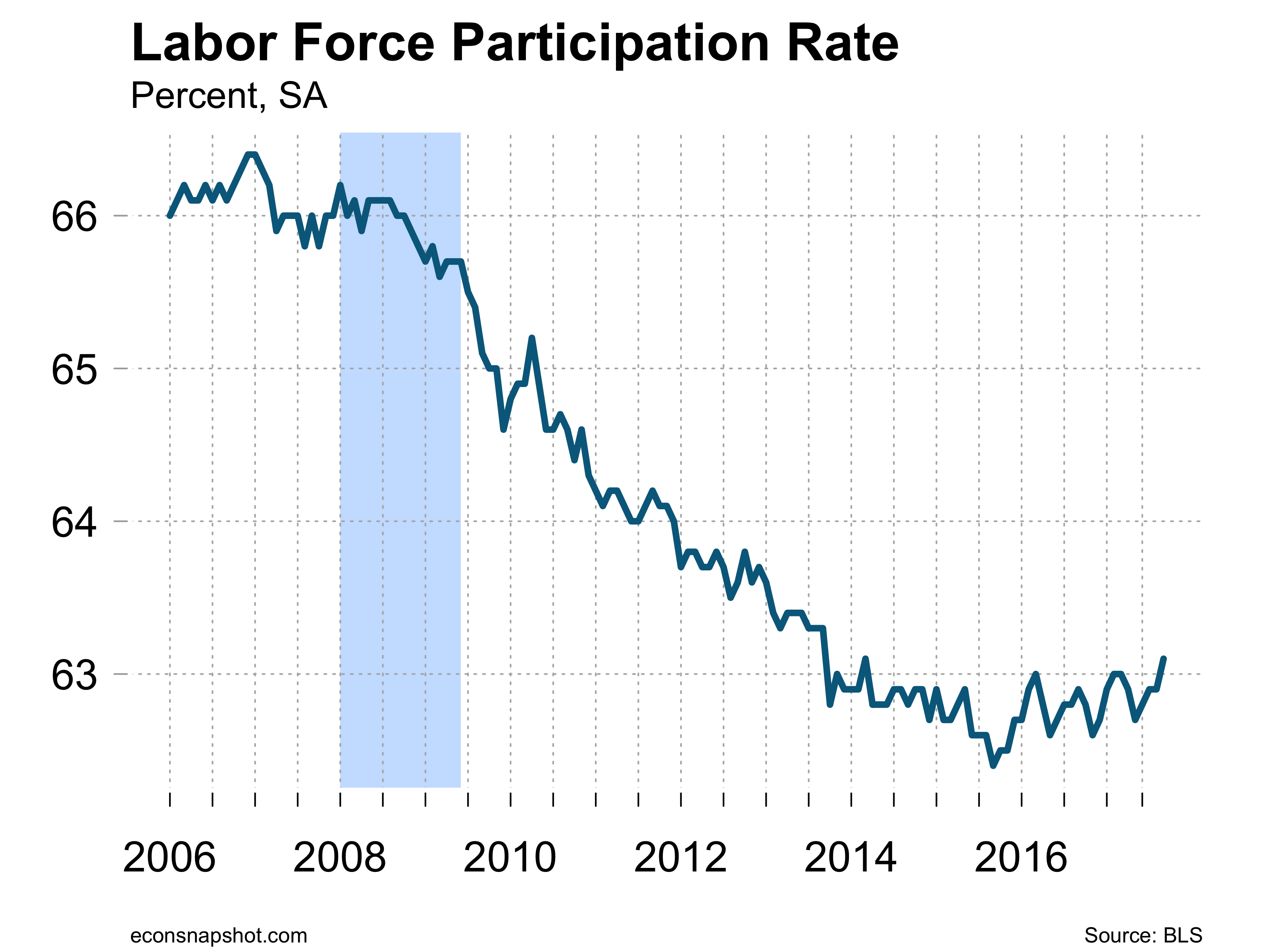

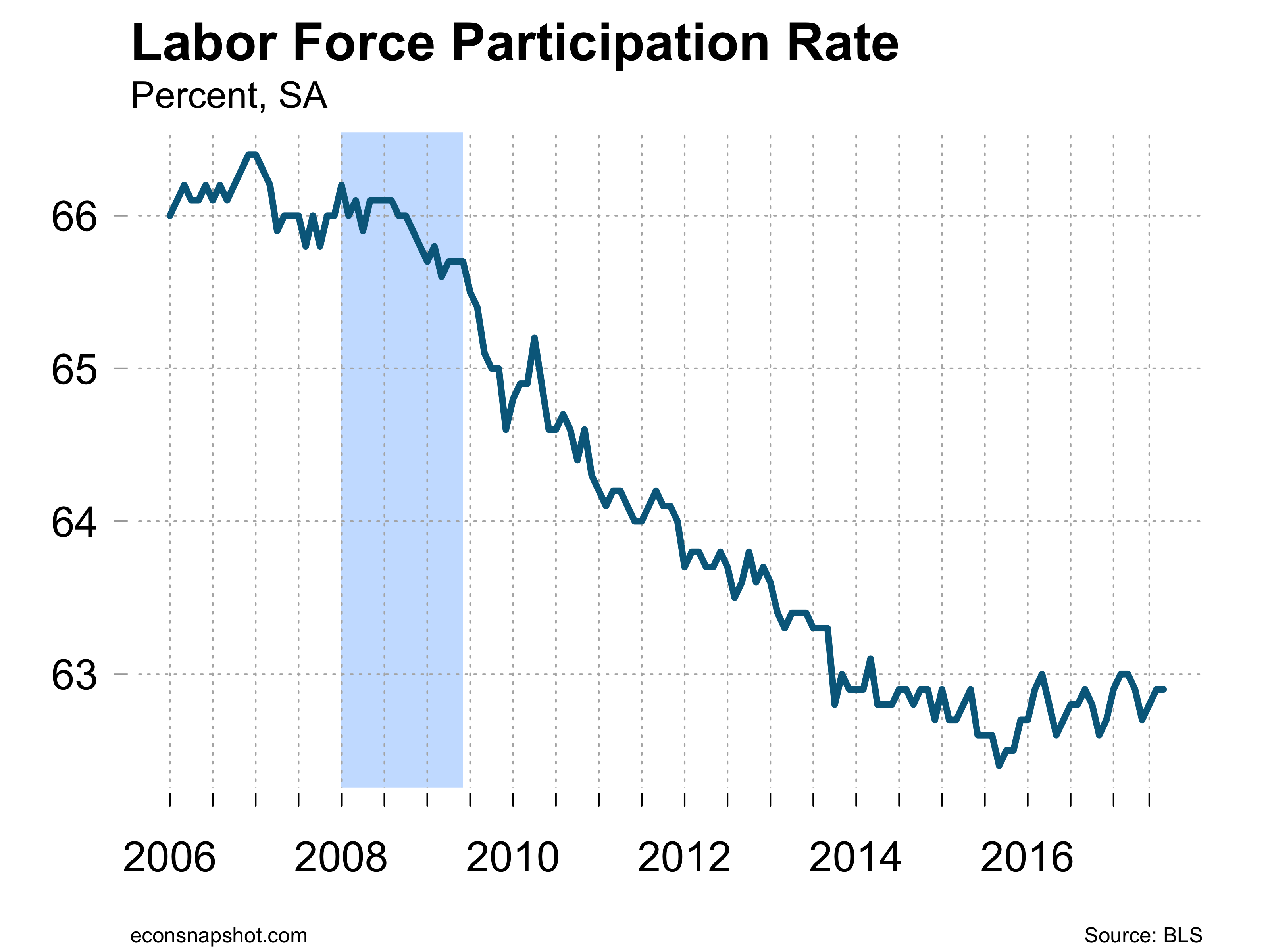

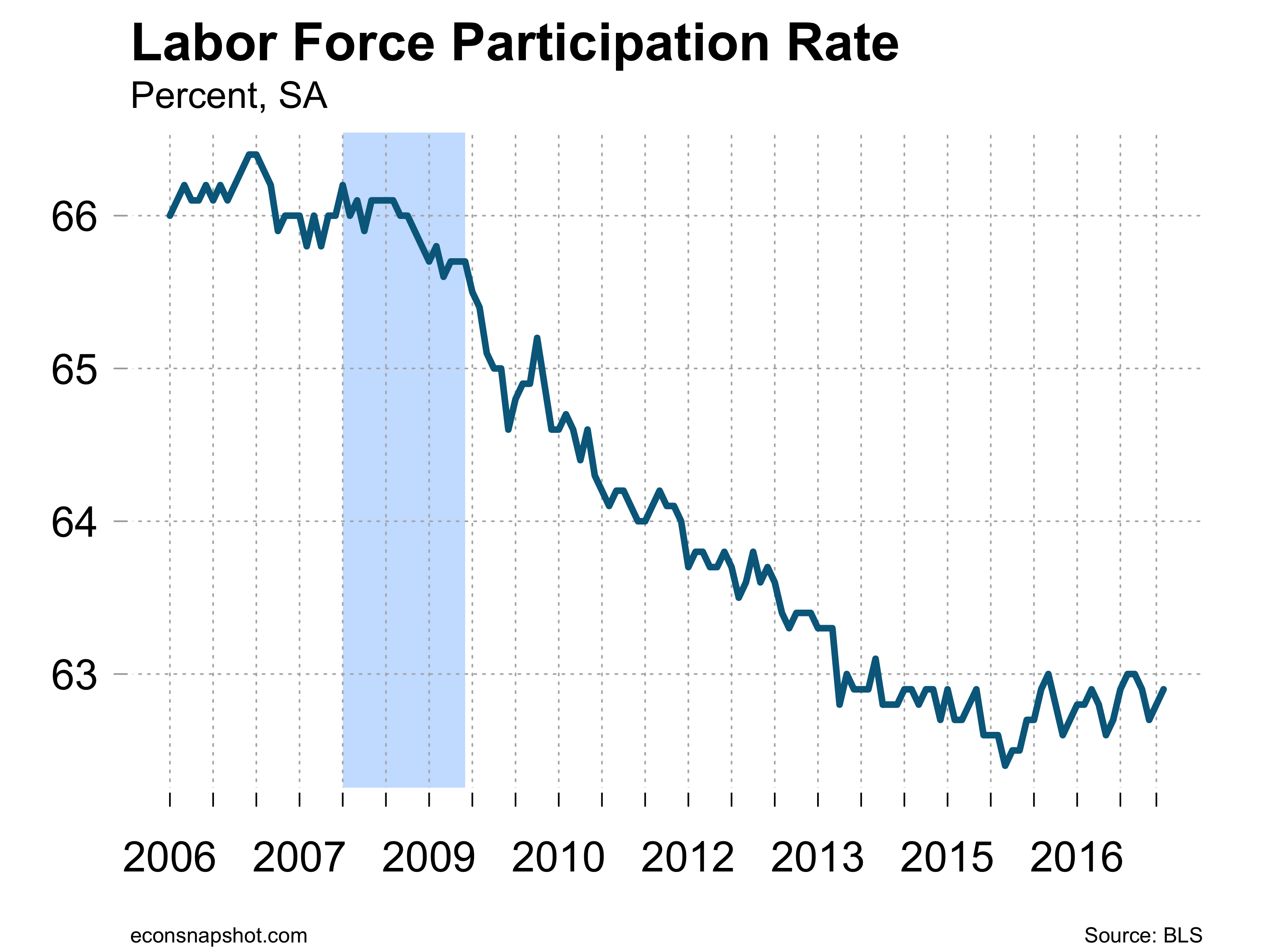

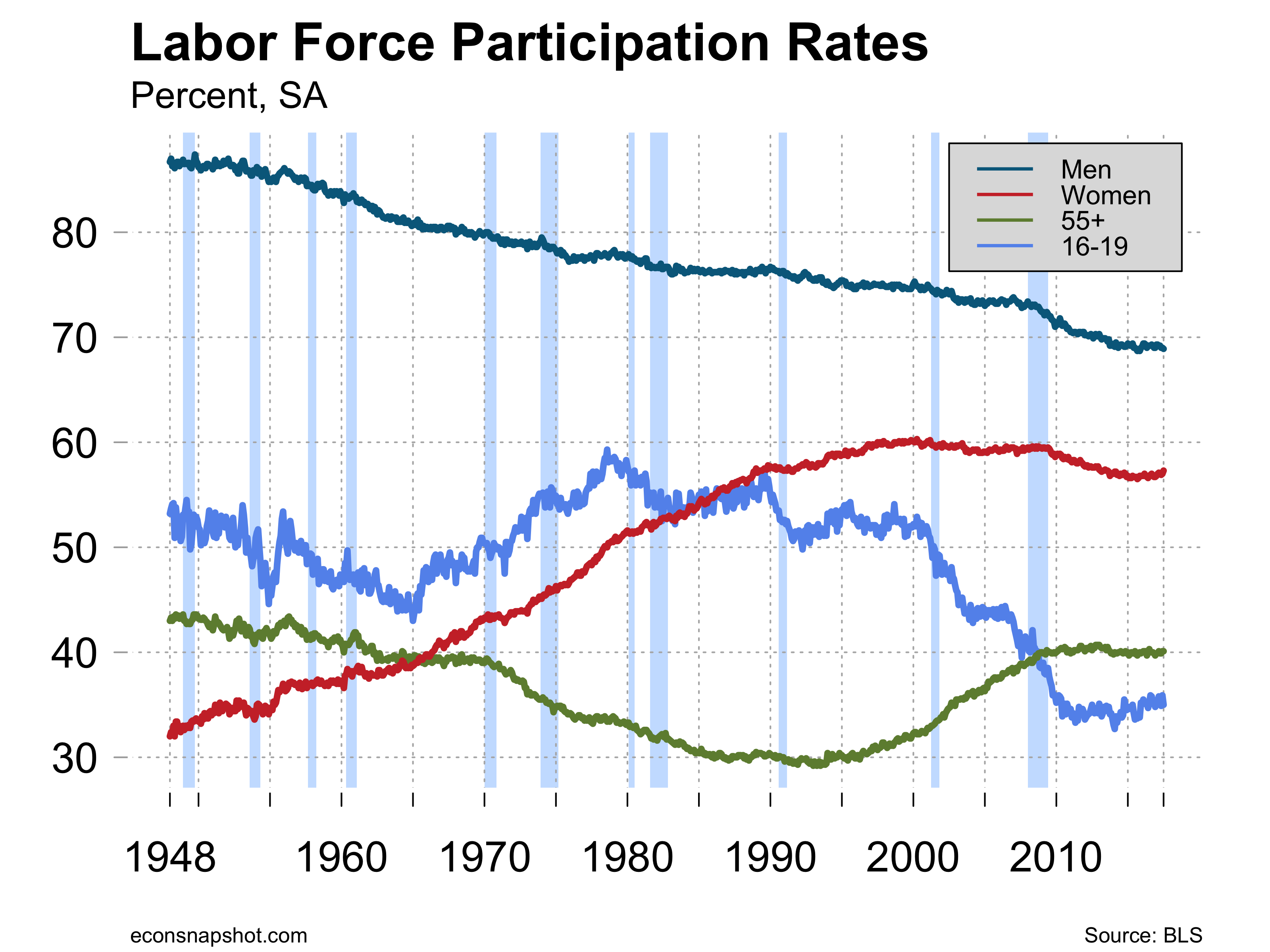

The labor force jumped up 361,000, leading to a small increase in the labor force participation rate to 62.8 percent about where it has been for the past year. The labor force participation rate for teens has been ticking up slightly, now at 35.9 compared to a series low of 32.7 in February of 2014. The labor force participation rate for men, women and those over 55 all have pretty much flattened out over the past couple of years.

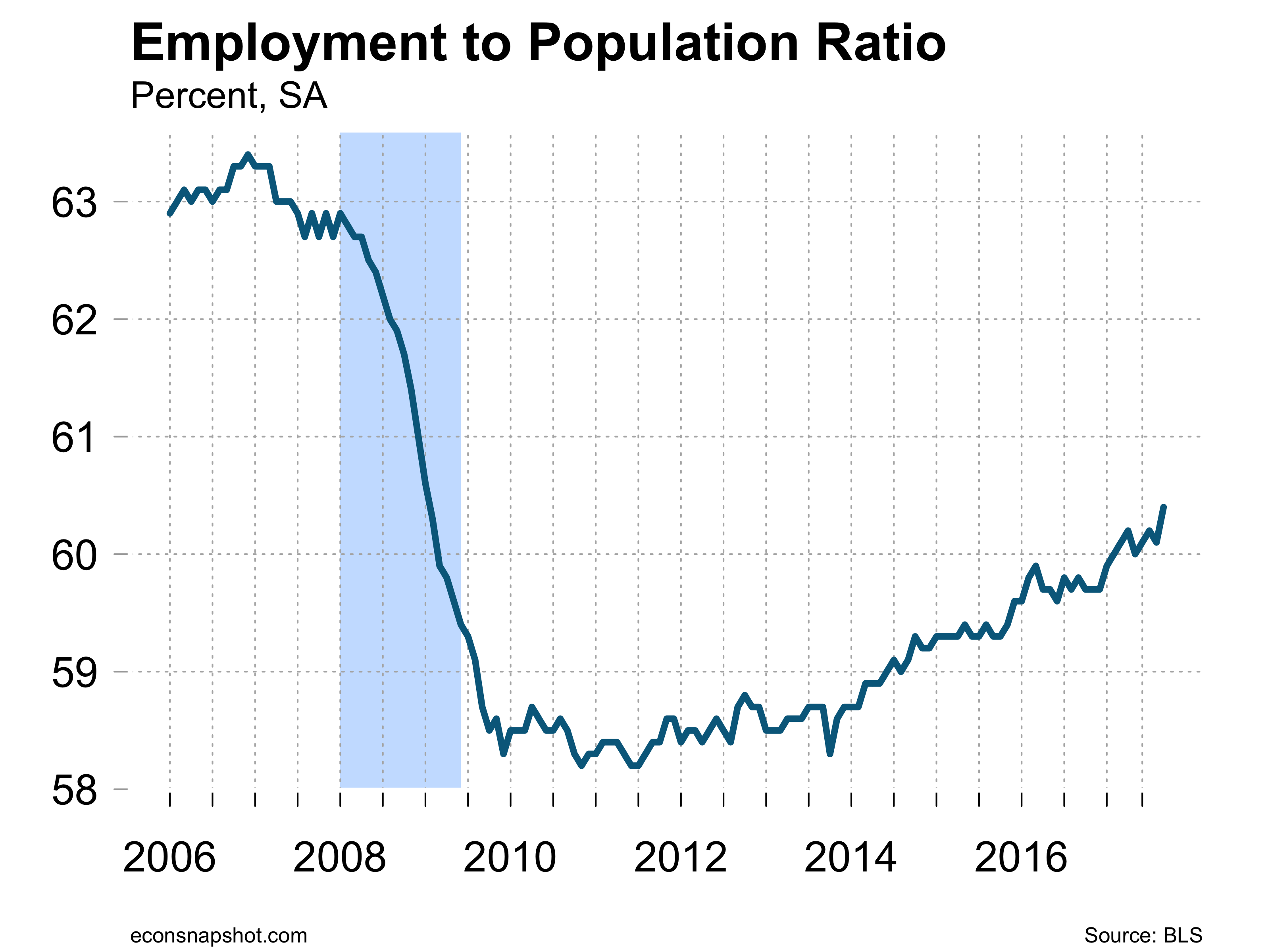

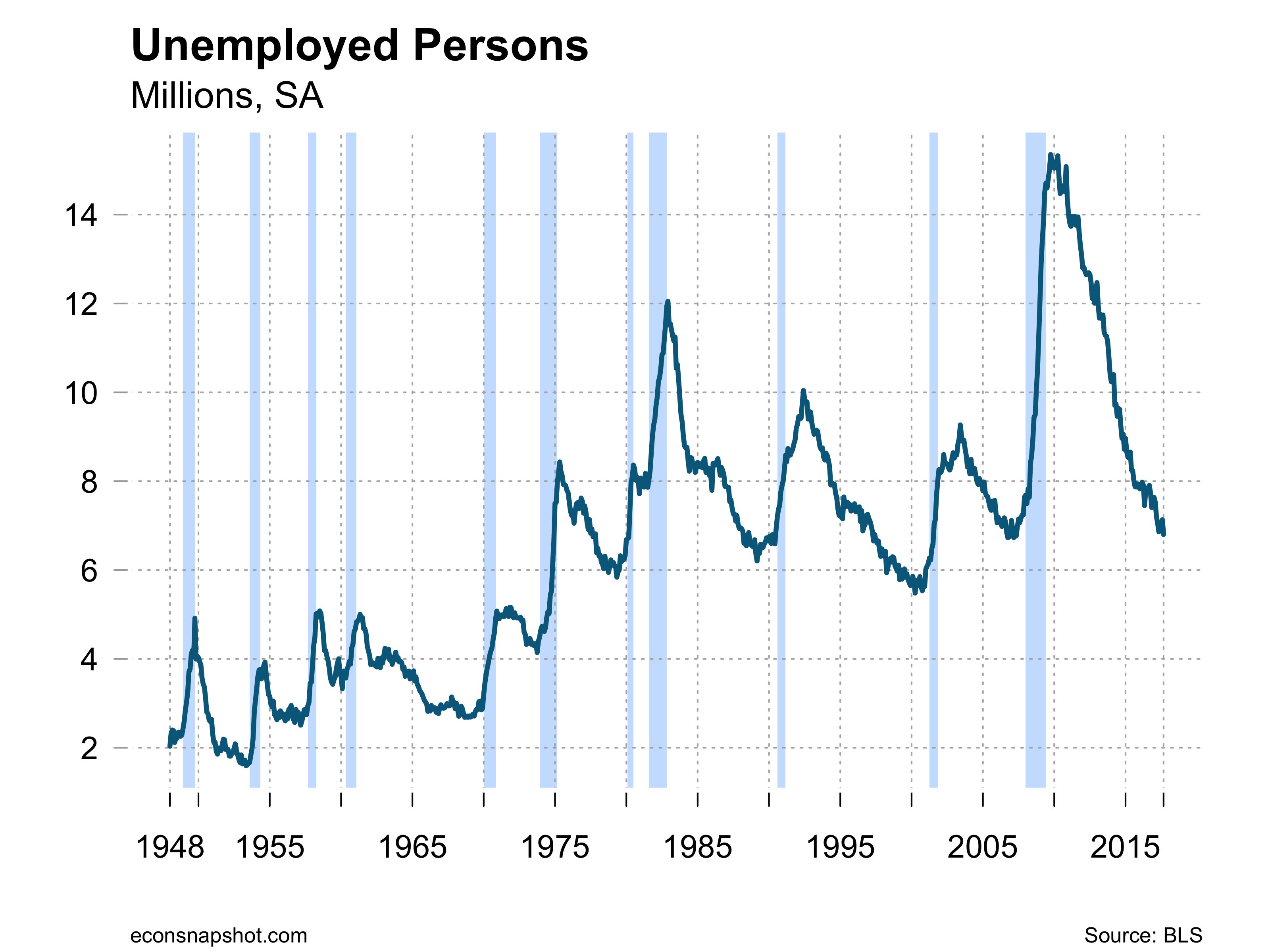

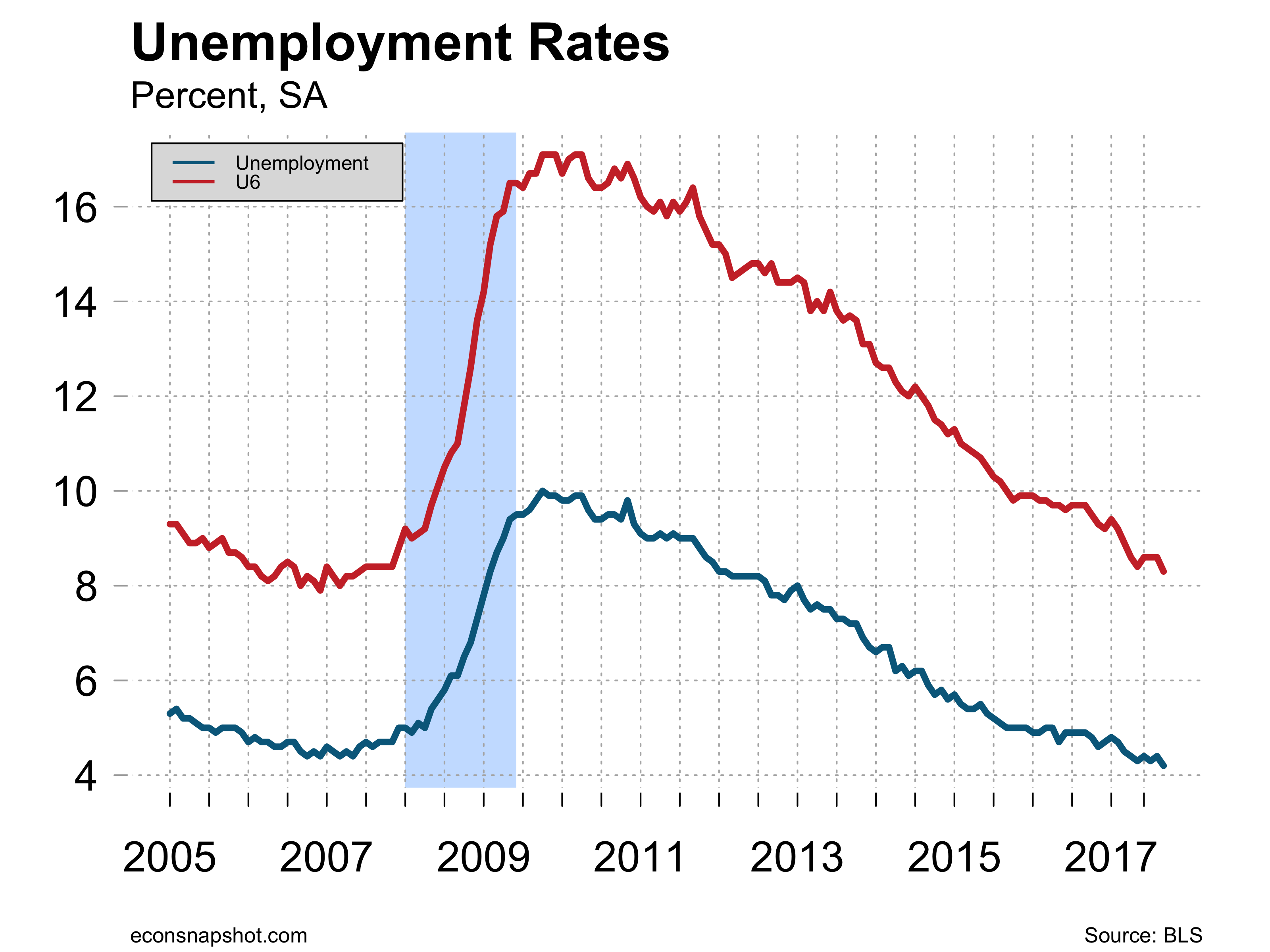

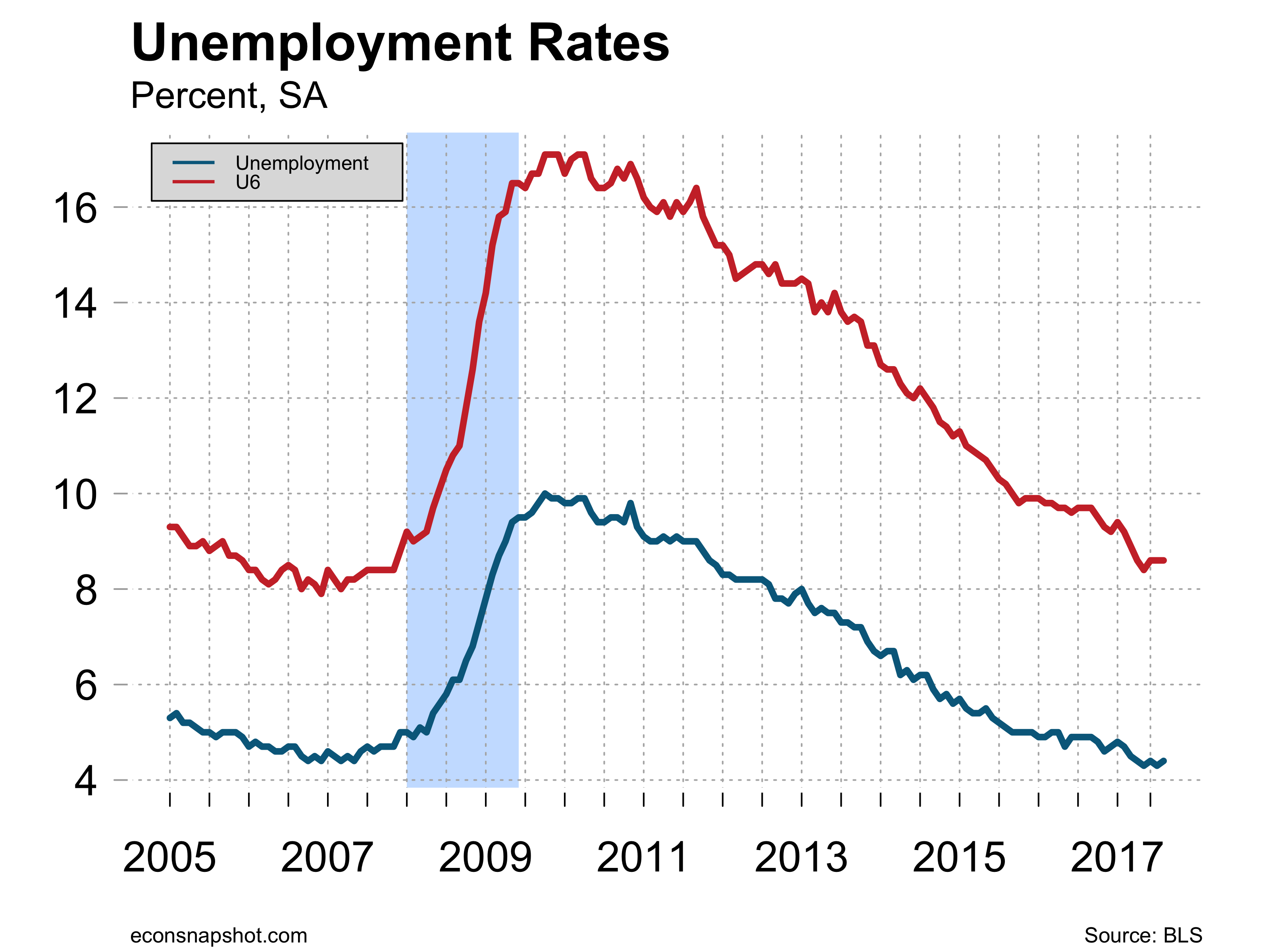

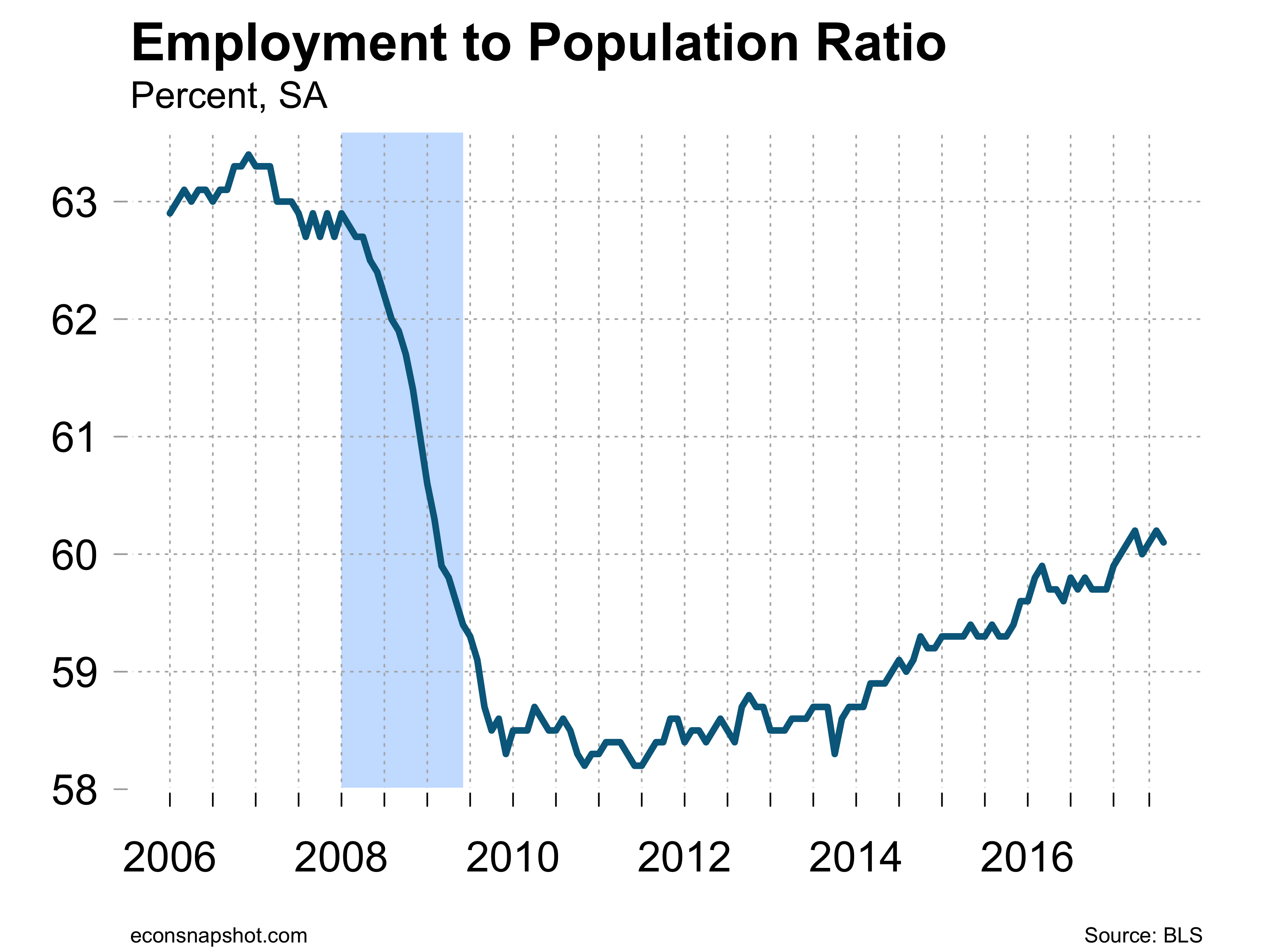

The number of persons unemployed was stable at 7 million. The employment to population ratio was also stable at 60.1 percent. The unemployment rate ticked up slightly, from 4.29% to 4.36%.

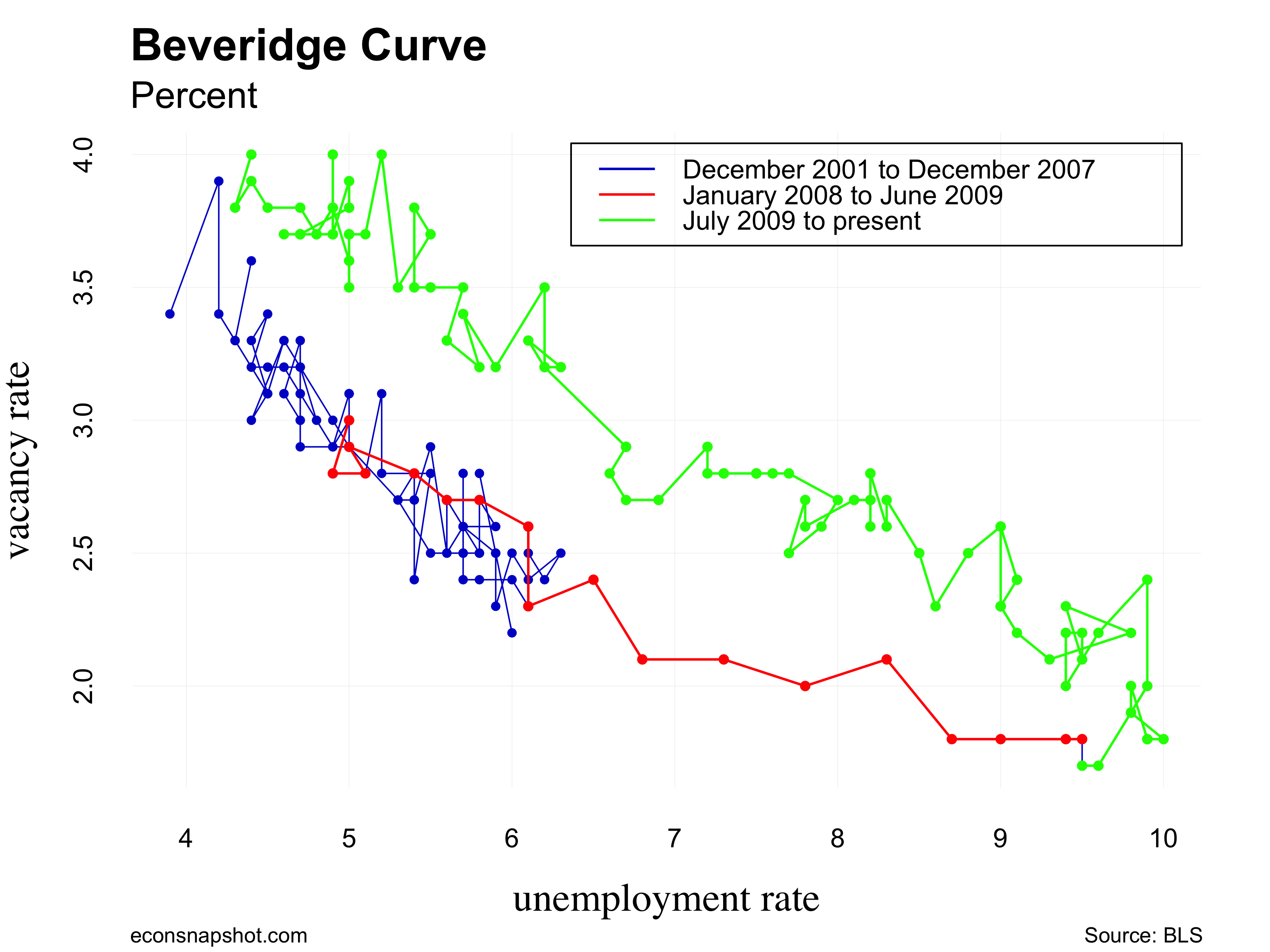

The Jobs Opening and Labor Turnover Survey shows that openings are at an all time high although the rate of hiring has slowed somewhat.

Where does this leave us? The Fed has mentioned at least one more rate increase for the year, yet the labor market is giving somewhat mixed signals. Employment continues to grow, sure, but wages continue to stagnate. There is much talk about the unemployment rate being at a record low but there is little reason to boast about this when labor force participation, and the employment population ratio remain at sucet.h low levels. This together with the stagnant wages and unfilled vacancies gives some support to the notion that there is a serious degree of mis-match in the labor market.